Municipals were mixed Monday ahead of a larger new-issue slate while U.S. Treasuries improved and equities were up near the close.

Triple-A yields saw a mix of one to two basis point bumps and cuts, depending on the curve, while UST saw yields fall by one to 11 basis points with the strongest moves inside 10 years.

Municipal to UST ratios rose slightly as a result. The two-year muni-to-Treasury ratio Monday was at 61%, the three-year at 62%, the five-year at 63%, the 10-year at 66% and the 30-year at 88%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 60%, the three-year at 61%, the five-year at 61%, the 10-year at 65% and the 30-year at 89% at 4 p.m.

This week should see a return to more normal supply, which might be a little higher than average for the year so far, said Daniel Solender, partner and director of tax-free fixed income at Lord Abbett & Co.

“Market technicals suggest average relative value in shorter maturities and better value out longer due to the upward sloping yield curve on the long end,” Solender said. “Overall trends depend upon macroeconomic indicators but the sentiment in the municipal bond market is stable.”

However, this week’s building calendar loses some relevance given the sparse supply last week, said Jeff Lipton, head of municipal credit and market strategy and municipal capital markets at Oppenheimer & Co.

Despite heavy reinvestment needs, retail has been fairly quiet, he said.

“Institutional interest remains committed on the front-end where cash is being deployed and bids are active,” he said.

This week’s tone will be heavily driven by June’s CPI report, which is largely expected to show moderating retail inflation, according to Lipton, who said there will be a continued active focus on this month’s FOMC meeting, with the current wager for a 25 basis-point rate hike expected.

“Issuer participation can be expected to recede ahead of the two-day session given a degree of rate anxiety normally associated with these meetings,” Lipton said. “While the thought of a rate decrease by year-end is out of the trade for now, sentiment ahead of the September meeting will likely be mixed.”

Despite the volatility that UST saw last week, Birch Creek Capital strategists said most “muni participants took an extended holiday break.”

“With just four trading days and many taking Monday off as well last week, secondary trading totaled to roughly $21.78 billion with 61% of trades being dealer sells,” said Jason Wong, vice president of municipals at AmeriVet Securities.

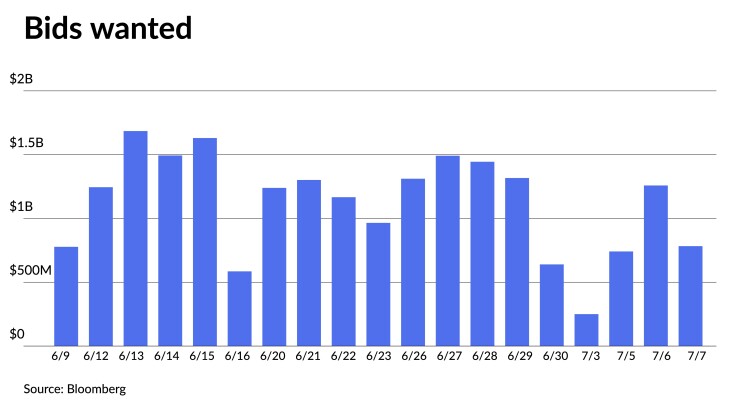

Bids-wanted was also down, with only $3 billion of bonds out for the bid, according to Bloomberg data.

With the Federal Deposit Insurance Corp. “sale process completed and very few new issues to raise cash for,” bonds available for sale dropped 54% on the week, Birch Creek Capital strategists noted.

“While the light calendar and holiday could be blamed for the lack of activity, traders also noted how accounts have been reluctant to adjust their offerings and willingness to sell relative to the actual bids being shown,” they said.

The AAA MMD curve was cut four to five basis points on Thursday “as accounts were finally forced to capitulate, however, the market was much weaker than that,” they said.

Stubborn holders appear “to be relying on the heavy influx of reinvestment cash relative to new supply, but with ratios approaching some of the lowest levels of the year, it will be hard for munis to outperform much further if rates continue their climb,” according to Birch Creek Capital strategists.

Wong pointed out the lower ratios, noting that with UST yields also rising, munis “continued to outperform Treasuries with 10-year notes now yielding 64.38% compared to 66.27% from the prior week.” One month prior, that ratio was at 70.15%, he said.

Since the start of June, munis “have been relatively unchanged for the most part with yields rising by an average of just 1.7 basis points,” he said.

Munis could continue to richen due to the Fed possibly raising rates another two times, he said.

Lipton said he continues to believe that munis are poised to outperform Treasuries for the year “and finish 2023 with modestly positive returns thanks to constructive technicals and the attractive absolute yield and cash flow opportunities, which strongly argue for duration extensions where feasible.”

In the primary market Monday, Raymond James & Associates priced for the Garland Independent School District, Texas (Aaa//AAA/), $145.315 million of PSF-insured unlimited tax school building bonds, Series 2023, with 5s of 2/2024 at 3.22%, 5s of 2028 at 2.86%, 5s of 2033 at 2.95%, 5s of 2038 at 3.43%, 4s of 2043 at 4.14% and 4s of 2045 at 4.20%, callable 2/15/2033.

Secondary trading

Washington 5s of 2026 at 2.97%. Columbus, Ohio, 4s of 2027 at 2.86%. Utah 5s of 2028 at 2.66%-2.65%.

Johnson County USD #229, Kansas, 5s of 2032 at 2.71%-2.68%.

Georgia 5s of 2040 at 3.25%. Dickinson ISD, Texas, 4s of 2041 at 4.10%.

Dickinson ISD, Texas, 4.125s of 2048 at 4.20%-4.32% versus 4.32%-4.33% original on Friday. Oklahoma Water Resources Board 4s of 2048 at 4.19%-4.18% versus 4.17% Friday and 4.14%-4.13% Wednesday.

AAA scales

Refinitiv MMD’s scale was cut up to two basis points: The one-year was at 3.09% (unch) and 2.97% (unch) in two years. The five-year was at 2.67% (unch), the 10-year at 2.64% (unch) and the 30-year at 3.56% (+2) at 3 p.m.

The ICE AAA yield curve was bumped up to one basis point: 3.06% (flat) in 2024 and 3.00% (flat) in 2025. The five-year was at 2.66% (-1), the 10-year was at 2.63% (-1) and the 30-year was at 3.62% (flat) at 4 p.m.

The IHS Markit municipal curve was cut up to two basis points: 3.09% (unch) in 2024 and 2.98% (unch) in 2025. The five-year was at 2.67% (unch), the 10-year was at 2.64% (+3) and the 30-year yield was at 3.56% (+2), according to a 3 p.m. read.

Bloomberg BVAL was cut up to one basis point: 3.05% (unch) in 2024 and 2.95% (unch) in 2025. The five-year at 2.65% (unch), the 10-year at 2.60% (unch) and the 30-year at 3.57% (unch) at 4 p.m.

Treasuries were firmer.

The two-year UST was yielding 4.868% (-7), the three-year was at 4.557% (-10), the five-year at 4.245% (-11), the 10-year at 4.003% (-6), the 20-year at 4.243% (-3) and the 30-year Treasury was yielding 4.038% (-1) near the close.

Primary to come:

The Denton Independent School District, Texas (/AAA/AAA/), is set to price Tuesday $969.940 million of PSF-insured unlimited tax school building bonds, Series 2023, serials 2024-2043, terms 2048, 2053. Piper Sandler & Co.

The Intermountain Power Agency, Utah (Aa3//AA-/), is set to price Tuesday $502.690 of tax-exempt power supply revenue bonds, 2023 Series A. Goldman Sachs.

The University of Southern California (Aa1/AA//) is set to price Tuesday $500 million of taxable corporate CUSIPs, Series 2023. Morgan Stanley.

The Public Utilities Commission of the City and County of San Francisco (Aa2/AA-//) is set to price Tuesday $412.040 million of San Francisco water revenue bonds, consisting of $346.975 million of 2023 Sub-Series A, serials 2028-2043, terms 2048, 2052, and $65.065 million of 2023 Sub-Series B, serials 2028-2043, terms 2048, 2052. Wells Fargo Bank.

The Louisville/Jefferson County Metro Government, Kentucky (/A/A+/), is set to price Tuesday $252.185 million of Norton Healthcare health system refunding revenue bonds, consisting of $145.290 million of Series 2023A and $116.895 million of Series 2023B. J.P. Morgan Securities.

The New Caney Independent School District, Texas (Aaa//AAA/), is set to price Wednesday $223.735 million of PSF-insured unlimited tax school building and refunding bonds, Series 2023. Piper Sandler & Co.

The San Diego Unified School District is set to price Wednesday $200 million of 2023-2024 tax and revenue anticipation notes, Series A, serial 2024. BofA Securities.

The Waxahachie Independent School District, Texas (Aaa//AAA/), is set to price Wednesday $200 million of PSF-insured unlimited tax school building bonds, Series 2023. Jefferies.

Grant County Public Utility District, Washington (/AA/AA/), is set to price Thursday $193.395 million of Priest Rapids Hydroelectric Project revenue and refunding bonds, Series 2023A. J.P. Morgan Securities.

Los Angeles (Aa2//AA/) is set to price Thursday $174.740 million of solid waste resources revenue bonds, Series 2023A. J.P. Morgan Securities.

The Connecticut Housing Finance Authority (Aaa/AAA//) is set to price Tuesday $146.940 million of social housing mortgage finance program bonds, Series 2023B, serials 2024-2035, terms 2038, 2043, 2048, 2053. Citigroup Global Markets.

The Michigan State Building Authority(Aa2//AA/) is set to price next week $114.085 million of Facilities Program multi-modal revenue bonds, Series I, term 2058. Barclays.

The Virginia Housing Development Authority (Aa1/AA+//) is set to price Tuesday $110.895 million of non-AMT rental housing bonds, Series 2023D, serials 2026-2035, terms 2038, 2043, 2048, 2053, 2058, 2065. Wells Fargo Bank.

The Chapel Hill Independent School District, Texas (/AAA//), is set to price Thursday $100 million of PSF-insured unlimited tax school building bonds, Series 2023. Piper Sandler & Co.

The New Mexico Mortgage Finance Authority (Aaa///) is set to price Thursday $100 million of tax-exempt non-AMT single-family mortgage program Class I bonds, Series 2023C, serials 2024-2035, terms 2038, 2043, 2048, 2053, 2054. RBC Capital Markets.

Competitive:

Seattle (Aa2/AA//) is set to sell $274.980 million of municipal light and power improvement and refunding revenue bonds, Series 2023A, at 10:45 a.m. eastern Tuesday.

The Broward County School District, Florida, is set to sell $200 million of tax anticipation notes, Series 2023, at 11 a.m. Tuesday.

Frisco, Texas, is set to sell $160.835 million of GO refunding and improvement bonds, Series 2023, at 10:30 a.m. eastern Wednesday.

Newport News, Virginia, is set to sell $101.535 million of GO general improvement bonds, Series 2023A, at 10:45 a.m. Wednesday.