Municipals were slightly weaker in spots Wednesday, largely ignoring the mixed reactions of other markets following the release of a hotter-than-expected consumer price index figure. The focus was on the primary where the Dormitory Authority of the State of New York priced for institutions with yields lowered by up to five basis points from the retail offering.

Equity indices and U.S. Treasury yields bounced from modest gains to modest losses, with equities ending mixed and USTs slightly firmer, noted José Torres, Senior Economist at Interactive Brokers.

“The tug of war between bulls and bears occurs as gasoline prices were the main culprit in [Wednesday’s] report,” he said.

“As bulls argue that gasoline is traditionally volatile, only up temporarily, and that price gains in some of the other categories slowed, bears insist that continued geopolitical tension is a significant feature of the 2020s inflationary landscape, one that warrants higher-for-longer interest rates,” Torres said.

He noted that Wednesday’s CPI report was not enough to “push September’s Fed meeting to live mode [but] November remains a tossup.”

There hasn’t been a huge return of capital in the muni market so far this year, with fund flows being rather anemic, said Chad Farrington, co-head of municipal bond strategy at DWS Group.

In the primary market Wednesday, BofA Securities priced for institutions $926.210 million of general-purpose state personal income tax revenue bonds, Series 2023A for the Dormitory Authority of the State of New York (Aa1/AA+//). The first tranche, $888.675 million of tax-exempts, saw yields bumped up to five basis points from Tuesday’s retail pricing: 5s of 2027 at 3.03% (-3), 5s of 2028 at 3.06% (-3), 5s of 2033 at 3.36% (unch), 5s of 2038 at 3.84% (-5) and 4s of 2042 at 4.30% (unch), callable 3/15/2033.

The second tranche, $37.535 million of taxables, saw all bonds price at par: 5.252s of 3/2033, 5.352 of 2034 and 5.67s of 2043, callable 3/15/2033.

In the competitive market, the Las Vegas Valley Water District (Aa1/AA//) sold $184.830 million of general obligation limited tax water bonds to BofA Securities, with 5s of 6/2027 at 3.03%, 5s of 2028 at 3.00%, 5s of 2033 at 3.12%, 5s of 2038 at 3.74%, 5s of 2043 at 4.06%, 5s of 2049 at 4.28% and 5s of 2053 at 4.35%, callable 6/1/2033.

The Dublin Unified School District, California, sold $145 million of Election of 2020 GOs, Series B, to Morgan Stanley, with 5s of 8/2024 at 3.10%, 5s of 2033 at 2.83%, 5s of 2038 at 3.39%, 4s of 2043 at 4.06%, 4.125s of 2049 at 4.24% and 4.25s of 2053 at 4.34%, callable 8/1/2033.

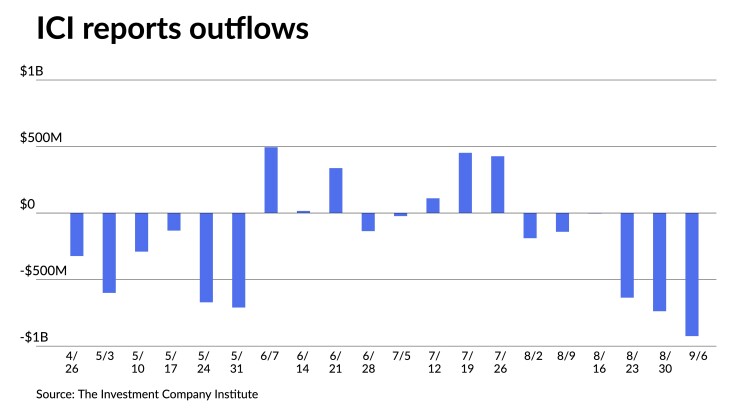

The Investment Company Institute Wednesday reported investors pulled $925 million from municipal bond mutual funds in the week ending Sept. 6 after $738 million of outflows the previous week. ETFs saw outflows of $222 million after $975 million of inflows the week prior.

There was a lot of tax-loss swapping last year where people “where selling the funds that they were losing, and they’re going into ETFs and we were told it may come back into the funds,” Farrington said.

However, he said he’s not sure that transition is happening, believing it may be more of a permanent transition where people leave muni mutual funds and go into lower-cost ETFs.

Additionally, the other factor is “it’s a distraction from Treasuries,” he said.

“You can get four and a quarter, four and a half at a high yield savings account. You can get five and a half on a six-month T-bill, so why do I bother with munis?” he said.

This could be a lag “as we’ve seen this before,” he said.

People are “piling into T-bills and taxable instruments and then they get their tax bill next year and said, ‘Whoa,'” he said.

From there, people may move into munis because even though they “may get a three and a half, four percent, which doesn’t sound as good as five or five and a half, but after tax, it actually is better,” Farrington said.

Additionally, as Treasury volatility ”bounces around,” he said people are sitting on cash.

Once the Federal Reserve finishes hiking rates, which Farrington believes is almost done, there is a good opportunity for money to come back into the market, leading to stronger returns.

There is also still some good upside for returns in the muni market. While investment-grade munis are returning negative 0.22% for the month, they are positive year-to-date with returns at 1.37%.

There also has not been a lot of supply this year. Through the end of August, supply was down 15.1% year-over-year to $244.677 billion. Volume for the month of August was down 13% to $36.514.

While supply is down, there are certain pockets of demand, he said.

For some paper, such as the PSF-insured Texas school districts where there was almost too much supply, there is less demand, while others like Grand Forks, North Dakota’s $150 million of Altru Health System revenue bonds on Tuesday, see stronger demand.

“It’s spotty,” Farrington said.

Muni-UST ratios on the front end of the curve are rich, historically speaking, he said.

The two-year muni-to-Treasury ratio Wednesday was at 63%, the three-year was at 65%, the five-year at 66%, the 10-year at 71% and the 30-year at 91%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 65%, the 10-year at 70% and the 30-year at 91% at 4 p.m.

However, he said that is because of separately managed accounts.

“SMAs are in there. They’re buying heavy, they were buying 2022 when we were seeing massive flows out of the funds,” he said. “So there’s support in the front end that justifies that.”

Farrington also does not see ratios cheapening back to where they were any time soon.

Secondary trading

Connecticut 4s of 2024 at 3.39% versus 3.33% on 9/7. Oregon 5s of 2025 at 3.22% versus 3.28% original on Tuesday. Georgia 5s of 2026 at 3.08%.

Ohio 5s of 2028 at 3.05%. California 5s of 2028 at 3.00%. Washington 5s of 2029 at 3.01%-2.99% versus 3.02% on 8/28.

NYC 5s of 2034 at 3.36% versus 3.38% Tuesday. California 5s of 2034 at 3.15% versus 3.15% Monday and 3.18% original on Friday. NYC TFA 5s of 2035 at 3.43% versus 3.32% on 8/31 and 3.40% on 8/29.

Palm Beach County, Florida, 5s of 2045 at 4.10% versus 4.03%-3.89% on 9/5. Battery Park City Authority, New York, 5s of 2048 at 4.12%-4.09%.

AAA scales

Refinitiv MMD’s scale was cut up to two basis points: The one-year was at 3.25% (unch) and 3.13% (unch) in two years. The five-year was at 2.90% (+2), the 10-year at 3.00% (+2) and the 30-year at 3.94% (+2) at 3 p.m.

The ICE AAA yield curve was little changed: 3.28% (unch) in 2024 and 3.19% (unch) in 2025. The five-year was at 2.91% (unch), the 10-year was at 2.95% (-1) and the 30-year was at 3.94% (unch) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut up to two basis points: 3.26% (unch) in 2024 and 3.14% (unch) in 2025. The five-year was at 2.91% (+2), the 10-year was at 3.00% (+2) and the 30-year yield was at 3.93% (+2), according to a 3 p.m. read.

Bloomberg BVAL was cut up to a basis point: 3.25% (unch) in 2024 and 3.16% (unch) in 2025. The five-year at 2.88% (unch), the 10-year at 2.91% (+1) and the 30-year at 3.91% (+1) at 4 p.m.

Treasuries were slightly firmer.

The two-year UST was yielding 4.981% (-2), the three-year was at 4.652% (-2), the five-year at 4.390% (-2), the 10-year at 4.251% (-1), the 20-year at 4.527% (-1) and the 30-year Treasury was yielding 4.341% (flat) at 3 p.m.

Money market funds see inflows

Tax-exempt municipal money market funds continued a three-week inflow streak as $1.39 billion was added the week Sept. 11, bringing the total assets to $117.98 billion, according to the Money Fund Report, a weekly publication of EPFR.

The average seven-day simple yield for all tax-free and municipal money-market funds fell to 2.90%.

Taxable money-fund assets gained $20.99 billion to end the reporting week. The average seven-day simple yield for all taxable reporting funds rose remained at 5.02%.

NYS plans $543M of GOs, potential tender offer

New York State plans to sell $543 million of tax-exempt and taxable general obligation bonds at the end of the month, State Comptroller Thomas DiNapoli said Wednesday.

The state expects to sell $459.4 million of Series 2023A, 2023B and 2023D new money GOs for transportation, education and environmental purposes on Sept. 27.

The state also expects to sell $83.4 million of Series 2023C refunding GOs on Sept. 28 to refund some outstanding bonds to lower the state’s debt service. Some of the Series 2023C bonds may also include refundings under a tender offer, DiNapoli said.

CPI read highest since June 2022

August’s CPI report came in hotter than expected, as the “headline inflation read showed CPI increased 0.6% in August from a month ago, which was the highest reading since June 2022,” said Edward Moya, senior market analyst at The Americas OANDA.

The annual inflation reading was “a tick above expectations,” rising from 3.2% to 3.7%, he said.

“Inflation is like our ugly wart,” said University of Central Florida economist Sean Snaith. “It continues to persist, despite our best treatments, and means we may need a stronger medicine.”

“August saw a gain in core inflation, while increased gasoline prices helped push headline inflation even higher compared to the prior month,” said Phillip Neuhart, director of Market and Economic Research at First Citizens Bank.

“After a couple of benign core CPI prints, we have a modest upside surprise in the August report while surging gasoline prices boosted headline inflation,” said ING chief international economist James Knightley.

“The jump in topline inflation was expected, but the slight uptick in monthly core inflation is slightly more worrying given the Fed’s focus on the stickier components of the index,” said Morning Consult senior economist Kayla Bruun.

“Even as energy prices go up and down, the pace of reducing core inflation has slowed to a crawl,” Snaith said.

“The longer it lingers, the more likely high prices get entrenched in consumer expectations and make it harder to achieve that 2% inflation target,” he said.

“There still remains ground to cover in returning inflation to 2.0% on a sustained basis,” said Wells Fargo Securities senior economist Sarah House and economist Michael Pugliese.

Moreover, they noted that “progress in reducing inflation over the next 12 months is likely to be more difficult than the past 12 months.”

“The sizable drag on inflation from lower commodity prices has faded, while the pace of goods deflation is likely to slow with some initial froth worked off of vehicle prices,” Wells Fargo Securities economists said.

“The road back to the Fed’s inflation target is expected to remain bumpy as a result,” they said.

The Fed will “keep rates on hold at the September FOMC meeting next week and the data following the September meeting will keep the Fed from hiking further,” Morgan Stanley strategists said.

While the Fed will “still keep rates on hold in September … it means officials will almost certainly keep one final hike in their official forecasts, even though we don’t think they will carry through with it,” Knightley said.

The recent slowdown in inflation “should be enough to keep the FOMC from hiking further this cycle,” but with the path back to 2% likely to hold some further twists and turns, we expect rate cuts to still be a way out,” Wells Fargo Securities economists noted.

Primary to come

Charlotte (Aa3//AA-/) is set to price Thursday $372.115 million of Charlotte Douglas International Airport revenue bonds, consisting of $260.175 million of non-AMT bonds, Series 2023A, serials 2025-2043, terms 2048 and 2053, and $111.940 million of AMT bonds, Series 2023B, serials 2025-2043, terms 2048 and 2053. BofA Securities.

The Ohio Water Development Authority (Aaa/AAA//) is set to price Thursday $150 million of Ohio Drinking Water Assistance Fund sustainability revenue bonds, Series 2023A. Jefferies.

Competitive

Montgomery County, Maryland, is set to sell $280 million of consolidated public improvement bonds, Series 2023A, at 10 a.m. eastern Thursday.

Wichita, Kansas, is set to sell $113.875 million of GO temporary notes at 10:30 a.m. Thursday.

Chip Barnett contributed to this story.